Who is Thoma Bravo and why are they BUYING logistics aggregators?

Private Equity meets Ecommerce Logistics

Thoma Bravo announced last week that it’s one step closer to orchestrating it’s monster $12 billion merger between its portfolio company Auctane and the 3PL powerhouse WWEX Group. The press releases are full of corporate-speak about “synergies” and “AI-enabled end-to-end logistics solutions.”

But this isn’t just another merger. This is the latest, and perhaps most audacious, move in a calculated game being played by one of the most aggressive and successful software investors in the world. Given the size of the deal, I think we should ask ourselves:

Who Are These Guys?

Forget the polished website and the pictures of smiling executives. Thoma Bravo, founded by Orlando Bravo, is a private equity machine that has perfected the art of the software buyout. They manage over $181 billion in assets and have a simple, ruthless, and wildly profitable strategy: find a good software company, buy it, make it more profitable, and sell it for a huge return.

They are not logistics guys. They are software guys. And they see the fragmented, complex world of logistics technology not as a series of operational challenges, but as a massive opportunity for consolidation. As one Forbes writer put it when Thoma Bravo bought Coupa Software, they are the “Barbarians at the Gate” of the supply chain world. And now, they’re not just at the gate — they’re rebuilding Rome.

The Playbook, Step by Step

What Thoma Bravo is doing is a repeatable, five-step playbook they have run over and over again across the software industry. The Auctane/WWEX deal is just the latest chapter.

Step 1: Identify the Platform

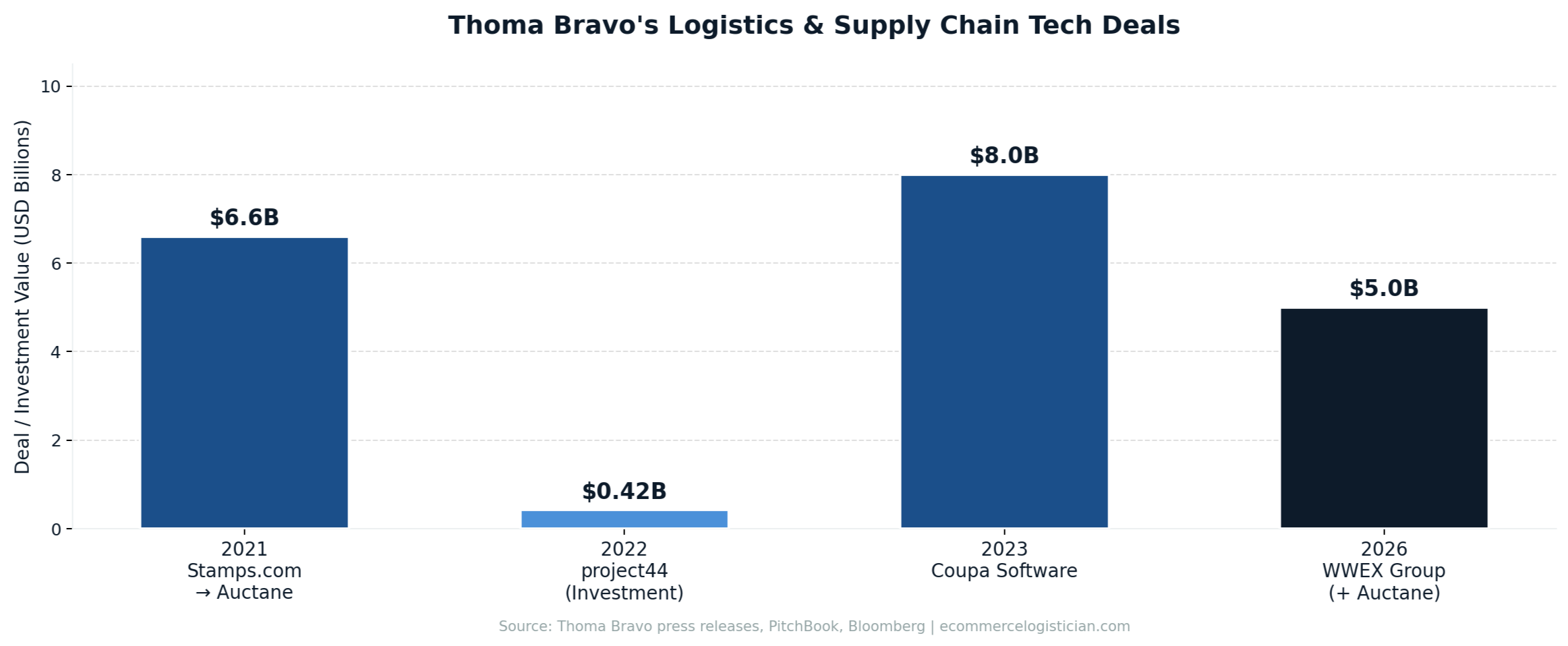

It starts with finding a market leader in a fragmented industry. The company needs to be good, but not too good. Maybe it’s inefficient, maybe its growth has stalled, or maybe it’s a public company struggling with quarterly earnings pressure. In 2021, they found their perfect platform: Stamps.com (formerly Nasdaq: STAMPS). For a cool $6.6 billion, they took the company private.

Step 2: Rebrand and Roll-Up

Once private, Stamps.com was rebranded as Auctane. This new entity became the “platform” for a classic “buy and build” strategy. Thoma Bravo used Auctane to go on a shopping spree, rolling up a huge chunk of the e-commerce shipping software market. ShipStation, ShippingEasy, ShipWorks, Metapack, Endicia — all these familiar names now live under the Auctane umbrella. Each acquisition consolidated their market power.

Step 3: Load It With Debt

Here’s where the financial engineering comes in. These deals are rarely paid for with cash on hand. They are leveraged buyouts (LBOs), meaning the acquired company is saddled with the debt used to buy it. For this latest WWEX merger, Thoma Bravo secured over $5 billion in a single unitranche financing deal from a syndicate of 33 lenders — including Blackstone, Ares, Apollo, and Oaktree.

This debt has to be serviced, which puts immense pressure on the newly formed company to cut costs and increase revenue. If that sounds familiar, it should. It’s the exact same playbook that killed Toys “R” Us. In 2005, KKR, Bain Capital, and Vornado bought the company for $6.6 billion, but loaded it with over $5.3 billion in debt. The interest payments alone — hundreds of millions of dollars a year — choked the company, preventing it from investing in its stores or e-commerce, and ultimately drove it into bankruptcy. The debt, not the business, is what wiped it off the face of the earth.

Step 4: The Grand Combination

After consolidating the software side, the playbook calls for a bigger move. By merging the pure-tech Auctane with the asset-heavy 3PL operations of WWEX Group — Worldwide Express, GlobalTranz, Unishippers — Thoma Bravo has created a vertically integrated behemoth. The new entity doesn’t just provide the software to print a label; it can now manage the entire journey from checkout to doorstep.

Step 5: The Exit

Private equity firms are not long-term holders. The end goal is always the exit. In a few years, expect Thoma Bravo to either sell this new, larger, more dominant entity to another company or take it public in a massive IPO. The $12 billion valuation is just the starting point.

The Broader Logistics Tech Takeover

To think this is just about one company is to miss the forest for the trees. Thoma Bravo is strategically buying up the key control points of modern logistics, and the scale of their investment is staggering. Between 2021 and 2026, they have deployed over $20 billion into just three major logistics tech platforms:

•Coupa Software (2023, $8 billion): A leader in business spend management with deep ties into supply chain and procurement.

•project44 (2022, $420 million investment, $2.2 billion valuation): The market leader in supply chain visibility.

•Auctane + WWEX (2026, ~$12 billion combined): The shipping software and freight brokerage combination.

The Elephant in the Room: Are These Companies Actually Tech?

Here’s the conversation that has been happening in boardrooms and at industry conferences for years, and one that this deal makes impossible to ignore any longer.

Auctane’s brands — ShipStation, Stamps.com, Endicia, ShippingEasy — belong to a category commonly called shipping aggregators. They sit between the shipper and the carrier, providing software to compare rates, print labels, and manage shipments. Competitors in this space include Shippo, Easyship, and EasyPost. On the freight side, the same model exists with companies like Flexport, and the now-defunct Convoy.

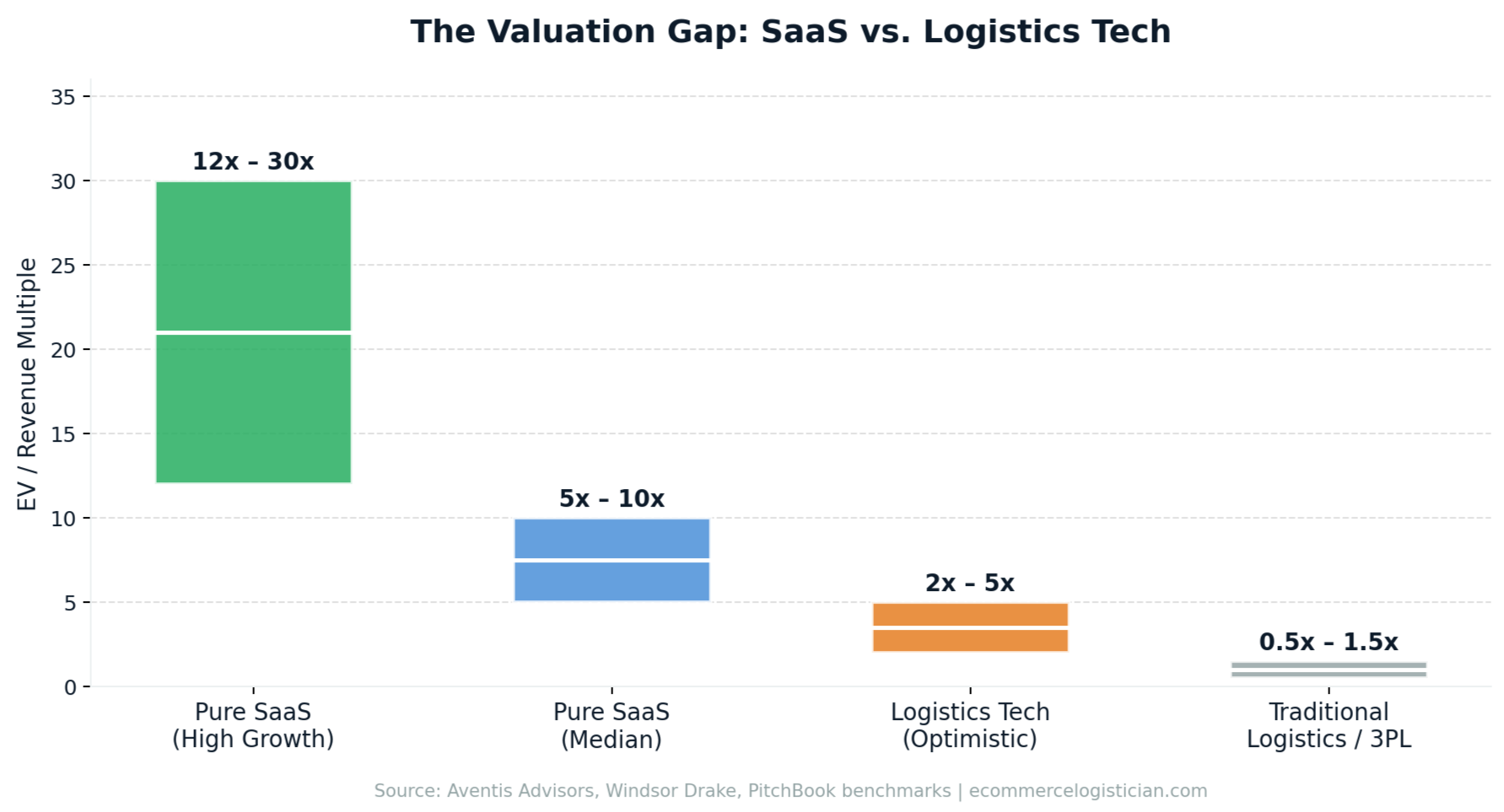

The fundamental question the industry has never been able to answer cleanly is this: are these businesses technology companies, SaaS companies, operations companies, or some hybrid of all three? And the answer matters enormously, because the category you land in determines your valuation.

Pure SaaS companies — the kind Thoma Bravo typically hunts — can trade at anywhere from 5x to over 20x revenue, depending on their growth. Traditional logistics companies, on the other hand, are lucky to get 1.5x revenue. The gap between those two numbers is enormous, and it’s the gap that has made the logistics tech space such a magnet for venture capital and private equity over the past decade.

The uncomfortable truth, however, is that the market has never — not once, in any sustained way — rewarded shipping aggregators and freight tech companies with genuine SaaS multiples. Not Stamps.com, which was consistently undervalued by public markets despite beating earnings expectations before Thoma Bravo took it private at $6.6 billion.

Not Flexport, which raised at a reported $8 billion valuation in 2022 and has been chasing profitability ever since. And certainly not Convoy, which raised $925 million, peaked at a $3.8 billion valuation in 2022, and was completely gone by October 2023.

Convoy’s story is worth dwelling on for a moment, because it is the clearest case study of what happens when a logistics company is valued like a tech company. The pitch was elegant: use machine learning to digitize freight matching the way Uber digitized rideshare. It worked beautifully during the COVID freight boom. Then spot rates collapsed by 40%+ in 2022 and 2023, and the entire model fell apart.

Convoy had no assets to fall back on, no physical capacity to leverage, and no relationship-based stickiness to retain shippers when the market turned. Flexport stepped in to buy the tech stack for pennies on the dollar. A tech company is not supposed to fall apart when shipping rates drops.

The pattern repeats itself across the industry. These companies start their lives positioned as technology companies, raise venture capital at tech company valuations, and then spend years trying to justify those valuations in a market that ultimately views them as logistics businesses. The boardroom debate about whether they are “tech” or “ops” is not just philosophical — it has real consequences for how these companies are funded, managed, and ultimately valued at exit.

This raises a genuinely interesting question, and one I don’t think anyone has a clean answer to: are these businesses structurally incapable of sustaining SaaS valuations, or have we simply not yet seen the right company execute the right model? The cousin industries — freight forwarding platforms like Flexport, digital freight brokerages like Convoy and Transfix — have all faced the same ceiling. Even the most tech-forward of them eventually gets repriced as a logistics business when the cycle turns.

The market is right to be skeptical. The economics of moving physical goods are fundamentally different from the economics of moving data. Gross margins in logistics are thin by nature. Customer acquisition is expensive. Churn is high because switching costs are low — a shipper can move from ShipStation to Shippo in an afternoon. And the business is brutally cyclical in a way that pure software never is. Until someone builds a shipping aggregator with 80%+ gross margins, 120%+ net revenue retention, and a defensible moat that doesn’t evaporate in a shipping price war, the market will keep applying a logistics discount.

So What Does This Mean for Thoma Bravo’s Bet?

Thoma Bravo is smart enough to know all of this. The question is whether they’ve found a way around it.

The thesis behind the Auctane/WWEX merger seems to be that combining the software layer with the physical freight, warehouse, and parcel layer creates something that is genuinely more defensible than either business alone. A shipper who uses ShipStation for their e-commerce labels and then routes their freight through Worldwide Express becomes stickier than a shipper who uses ShipStation alone. The data flywheel — knowing both the software preferences and the freight patterns of a customer — could theoretically create the kind of lock-in that justifies a higher valuation.

Whether that plays out in practice is a different question. The history of logistics mergers is full of deals that made perfect sense on a whiteboard and fell apart in execution. Remember Sendle in Australia — a promising company, a well-intentioned merger, and then a collapse that left thousands of customers scrambling. The $5 billion debt load sitting on top of this new entity is not forgiving. It demands results, and it demands them quickly.

For the thousands of small and medium-sized e-commerce businesses that rely on these platforms, the consolidation is a double-edged sword. In the short term, nothing may change. But in the long term, fewer choices, less competition, and almost certainly higher prices tend to follow when one company owns ShipStation, Stamps.com, ShippingEasy, and Metapack all at once.

This is the new reality of logistics tech. A world being reshaped not by operators in warehouses, but by financiers in boardrooms. And while it may be a brilliant playbook for generating returns, the final cost to the industry’s innovation and competitiveness has yet to be tallied.

If you’re looking for a guest speaker, analyst, or consultant for your project, company, or event, reach out.