Thoma Bravo planning $12B merger between Auctane and WWEX group

Pure genius or train wreck?

Private equity firm Thoma Bravo wants to merge portfolio company Auctane Group which includes Stamps.com, Endicia, ShipStation, Metapack, Packlink, and more, with logistics group WWEX which includes Global Express, GlobaTranz, and Unishipppers to form a $12 billion vertically integration logistics and logistics tech juggernaut.

Is this move pure genius? Or a train wreck waiting to happen? Read on!

The Proposed $12B WWEX Group

On the outside the plan sounds brilliant. Auctane owns several market leaders in the label aggregation business, has 1M ecom customers, and is firmly a technology company.

WWE on the other hand is a logistics operator providing freight forwarding, trucking, warehousing and fulfillment, and also label resale - notably being a strong UPS reseller - and boasts 121K customers of their own.

Combining the two sounds like the perfect vertical integration of technology and logistics with infinite possibilities.

Deal Structure

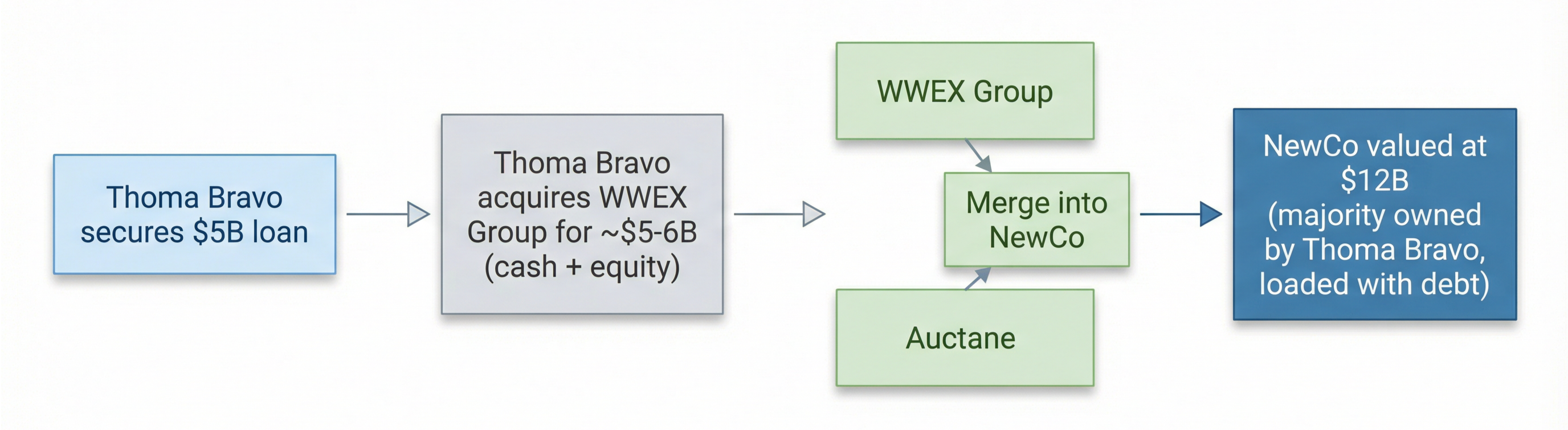

To know what’s really happening, let’s follow the money:

Thoma Bravo is taking a new $5B loan, giving it cash

Thoma Bravo uses (1) cash and (2) some equity in the combined new company to (3) buy WWEX from it’s current owners for about $5-$6B

Thoma Bravo then merges WWEX and Auctane together into a new company (or existing)

Thoma Bravo then injects additional $500M into the group either for equity or as a loan

After the dust settles, WWEX will probably have a lot of cash in hand, maybe some debt due to them, and some equity in the new combined company, while Thoma Bravo will own the majority of the combined new company, which is probably loaded with debt up to its eyeballs.

Auctane was acquired by Thoma Bravo in 2021 in a $6.6 billion privatization deal, previously trading as Stamps.com.

Therefore Auctane $6B + WWEX $6B = $12B value for the new combined company. Illustration as follows:

Thoma Bravo’s Auctane Problem

Because Thoma Bravo fought Auctane at the peak of the market for SAAS valuations, it likely cannot get a good return from listing the company again. The market that Auctane is in is a brutally competitive market. In the US alone, competitors include Shippo, Easypost, PitneyBowes, Vesyl, Easyship, ShipperHQ, and many more. This is not typical kind of SAAS business that Thoma Bravo invests into where these companies are throwing off massive predictable cash flow. Thoma Bravo needs to figure out what to do with Auctane.

The Problem With This Merger

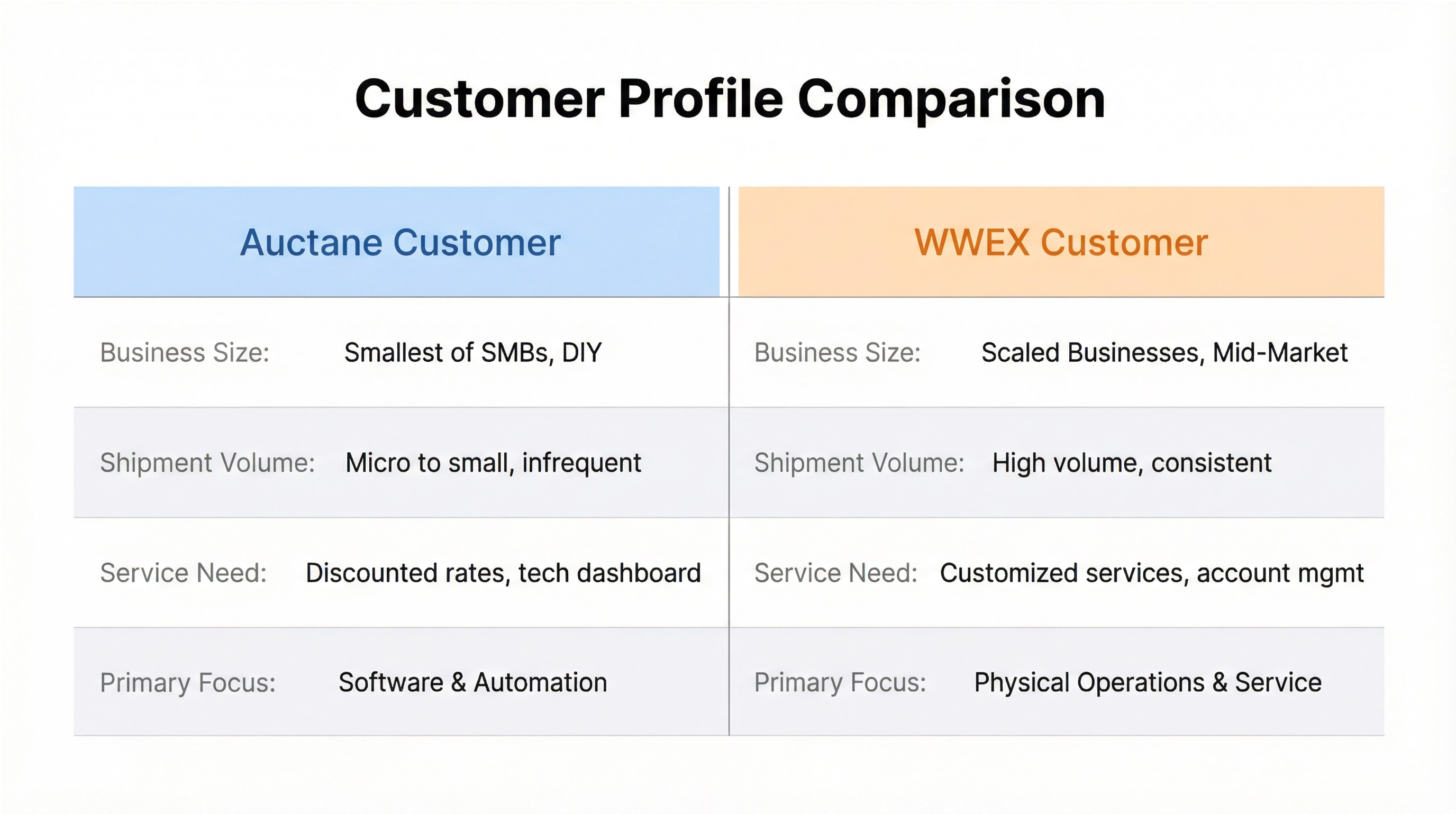

The biggest problem with this merger is that Auctane’s ICP is too different from WWEX’s.

Auctane services the smallest of SMBs, typically Shopify Core, Woocommerce, Wix, and other SMBs looking for a access to discounted carrier rates, a great dashboards and tech, rate comparisons, and a number of different value adds depending on which brand we are talking about. Their customers have micro to small volumes, infrequent shipments, and are very hands off DIY. Yes of course they have mid market and enterprise too.

WWEX customers, however, are the opposite. They are more scaled businesses that want customized services, high touch account management, and physical operations and services dominate their needs.

Trying to force Auctane customers into WWEX’s services would be painful for both parties, and WWEX customers don’t need Auctane.

History Lesson: Deliverr and Shipwire

Trying to merge tech companies with physical logistics companies has failed big time before.

Shopify acquired fulfillment company Deliverr for $2.1 billion in 2022 and that failed spectacularly, resulting in Shopify cancelling it’s Shopify Fulfilment program and selling Deliverr to Flexport for no cash and just a 13% stake in Flexport. You can read about why they failed from this Modern Retail article.

Shipwire is another tragedy to learn from. One on the first tech logistics companies, it was sold to Ingram Micro, a traditional distribution business, in 2013 where it languished until it was sold to CEVA logistics where it further declined into market irrelevance and it was just sold recently again to Stord. While there’s been no long expose that I could find on why it failed, anyone who has worked in traditional logistics knows that

What Would You Do

There are only a few major business model trends that fundamentally change the game for logistics companies right now:

Out of Home

Quick Commerce

AI and Automation (not just implementing, but being a tech company)

The first 2 are out of reach given the new WWEX Group’s lack of last mile. The only thing that would remain is whether Auctane’s engineering prowess, which is significant, can be redeployed into turning WWEX’s business into an organization that more resembles Cainiao or Amazon with a tech first culture, mindset, and management.

Frequently Asked Questions (FAQ)

1. So, what exactly is Auctane and who owns it?

Think of Auctane as the massive, quiet giant behind the shipping labels for millions of small e-commerce businesses. It’s not one single brand but a portfolio company owned by the private equity firm Thoma Bravo. Auctane itself owns a whole family of shipping software you’ve definitely heard of: ShipStation, Stamps.com, Endicia, ShippingEasy, ShipEngine, and Metapack, among others. Thoma Bravo took the company (then called Stamps.com) private in a $6.6 billion deal back in 2021, right at the peak of the SaaS valuation craze. Essentially, if you’re an online seller printing labels, there’s a good chance you’re an Auctane customer whether you know it or not.

2. And what about WWEX Group?

WWEX Group is the other side of the coin. While Auctane is a pure technology company, WWEX is a logistics operator. They are a massive third-party logistics (3PL) provider, one of the largest non-retail resellers of UPS services in the US. The group itself is a combination of Worldwide Express, GlobalTranz, and Unishippers. Their bread and butter isn’t small, DIY online sellers. Their customers are more scaled businesses that need high-touch account management, freight brokerage (like LTL and truckload), and customized shipping solutions. They move a ton of volume and have deep relationships with carriers.

3. What’s the real valuation of Auctane and this new merged company?

The headline number being thrown around is $12 billion for the combined entity. Here’s the napkin math: Thoma Bravo bought Auctane for about $6.6 billion. WWEX Group is being valued in this deal at roughly $5 to $6 billion. Add them together, and you get to that $12 billion figure. However, the real valuation is a much murkier question. Thoma Bravo likely overpaid for Auctane in 2021 and is now sitting on an asset that’s hard to flip for a profit in today’s market. This merger is a creative way to restructure, load the combined company with new debt (a fresh $5 billion loan), and create a new story for investors. The true enterprise value will depend entirely on whether this forced marriage actually creates any real synergies, which, as I argued, is highly questionable.

Side Note: I got challenged on LinkedIn by an ex-MetaPack employee saying that I didn’t know what I was talking about saying that Auctane doesn’t do Enterprise. He’s right. MetaPack is famously Enterprise, but they are the lone wolf in the pack, and desperately clinging onto an outdated legacy model that isn’t suited to the next generation buyer.

4. What does this merger really mean for the average ShipStation customer?

In the short term? Probably not much. Your ShipStation dashboard will look the same, and your discounted USPS rates won’t disappear overnight. But in the long term, the strategic fit is awkward. Auctane’s customers are small, hands-off, DIY shippers. WWEX’s customers are larger businesses that want managed services. The risk is that Thoma Bravo will try to force a clumsy integration, pushing expensive contract logistics and freight services onto small sellers who don’t need them, or trying to automate WWEX’s high-touch service model, potentially alienating their core customers. The key risk is a period of internal confusion and strategy shifts that could distract from innovation and customer service for both sides.