Why is Stord acquiring so many 3PLs?

And will they acquire even more.

Who is Stord

Stord, founded in 2015 by Sean Henry and Jacob Boudreau, has raised $527 million and is today one of the fastest growing ecommerce fulfillment companies in the world, valued at $1.5 billion. It has also made 8 acquisitions in the past 6 years.

Customer wise, it generally targets small to medium sized DTC ecommerce businesses, although it also services a number of enterprise level clients.

What is particularly notable about Stord isn’t it’s revenue, size, or footprint, but it’s positioning and strategy.

While Stord appears to be a 3PL (ie fulfillment) company, it’s positioned itself as a technology company to investors - a business that is at it’s essence a software cum hardware technology company which uses it’s technology to run, operate, and orchestrate various ecommerce fulfillment services.

As such, it’s been able to raise venture capital at generous valuations, giving it access to cheap and abundant capital, which it has in turn deployed heavily towards acquisitions.

It’s frequency 1 or more acquisitions per year imply that acquisitions are a core part of it’s growth and fundraising story.

Stord’s Acquisition History

June 2020 - Cove Logistics

Freight broker based in Springfield Missouri adding brokerage capabilities to it’s warehousing marketplace. Deal valued at sub $10M. Initial Covid shock.

September 2021 - Fulfilment Works

This traditional warehousing and fulfillment provider marked Stord’s entry into direct ownership and operation of physical logistics. With the world in lock-down, Ecommerce was booming worldwide.

April 2024 - ProPack Logistics

Cold-chain specialist servicing nutrition, supplement, health and beauty verticals. During the same time, Lineage, another cold chain logistics company, IPO’s at a $19 billion valuation, thrusting cold chain into the spotlight.

July 2024 - Pitney Bowes Ecommerce Fulfillment

Opportunistic acquisition by Stord. Pitney Bowe’s (PB) Global Ecommerce (GEC) and Ecommerce Fulfilment businesses had been in distress due to USPS termination of the DDP program which was the bedrock of PB’s ecommerce business. PB traditionally serviced mid-market and enterprise brands. Stord acquires PB’s massive 640,000 sq ft facility in Kentucky.

May 2025 - Ware2Go (via UPS)

Acquired from UPS, adding 21 more fulfillment centers and 2.5 million sq ft of warehouse space. Ware2Go was positioned more for the ecommerce SMB/SME market.

July 2025 - Penny Black

A technology company enabling personalised inserts and unboxing experiences for brands and retailers.

January 2026 - Shipwire (via CEVA)

Acquired from CEVA logistics, who acquired it from Ingram Micro, adding 12 more fulfillment centers, including strong international presence, and an in-house technology platform for warehousing and fulfillment that had been continuously improved for more than a decade.

February 2026 - Quiet Logistics (via American Eagle Outfitters)

Another opportunistic acquisition by Stord. Acquired from American Eagle Outfitters (AEO) who had themselves acquired Quiet Logistics with the intention of developing Quiet into a major logistics and supply chain service provider in the apparel industry. AEO’s investment was a failure, leading to the public announcement of Quiet’s winding down, at which point Stord assumed the lease and other assets of the Quiet business.

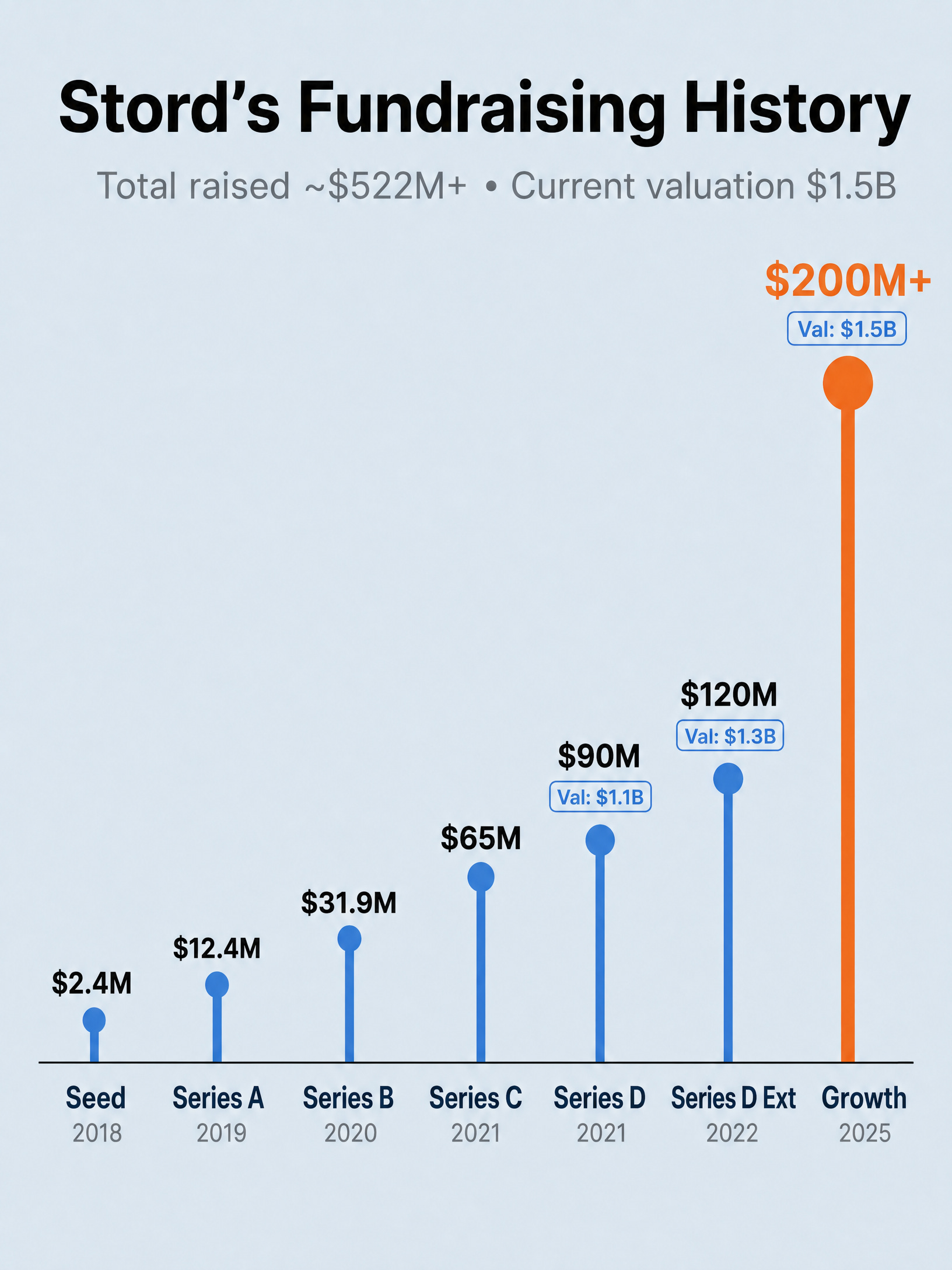

Stord’s Fundraising History

For a startup of Stord’s size and history, acquiring other companies at this frenzied pace is unusual. In order to understand why it’s doing this, you have to first look at it’s fundraising. To date Stord has raised approximately $527M and was last valued at $1.5 billion.

April 2018 — Seed Round: $2.4M, Valuation: Undisclosed

Investors: Susa Ventures, Dynamo Ventures. Revolution, Engage, Chris Klaus

June 2018 — Angel Round, Amount and Value: Undisclosed

Investor Tom Noonan

March 2019 — Series A: $12.4M, Valuation: Undisclosed

Investors: Kleiner Perkins, Susa Ventures, Revolution, Engage, Dynamo Ventures.

November 2020 — Series B: $31.9M, Valuation: Undisclosed

Investors: Founders Fund, Dynamo Ventures, Kleiner Perkins, Susa Ventures, Good Friends, B Capital

March 2021 — Series C: $65M, Valuation: Undisclosed

Investors: Bond Capital, Founders Fund, Susa Ventures, Dynamo Ventures, Salesforce Ventures, Lineage Logistics. Yes the same Lineage mentioned earlier.

September 2021 — Series D: $90M, Valuation: $1.1B

Investors: Franklin Templeton, Bond Capital, Founders Fund, Kleiner Perkins.

April 2022 - Seires D Extension: $120M, Valuation $1.3B+

Investors: Franklin Templeton

March 2025 — Equity and Debt Round: $200M, Valuation: $1.5B

Debt means loans, which likely take on interest and requirement repayment. This is not uncommon in later stage companies that can service debt from operating cash flows.

Companies positioned as a high growth tech companies can raise money at premium valuations. Hypothetically, a company like Stord, when positioned as a logistics tech platform, might raise new money at 10x revenue.

At the same time, a traditional fulfillment company like Quiet Logistics might only be valued at 1x revenue, or more precisely probably 3x-5x earnings.

This presents an immediate arbitrage opportunity.

Example of Fundraising M&A Arbitrage

Startup with $10M in revenue is valued at 10x revenue, or $100M, and raises $25M new money

Startup uses $25M to acquire a traditional logistics company with $25M in revenue

Startup $10M revenue + Acquired Company $25M = $35M in combined revenue

Startup is now valued at 10x revenue, or $350M, an valuation increase of $150M

Repeat

The Elephant in the Room

The question future investors will be asking is whether Stord should continue to receive the premium valuations of a tech company, or whether it’s really a logistics company.

Since Stord markets, sells, manages, and operates physical warehouses, it is no longer a pure technology company, but it can still be considered a hybrid.

The track record for well funded logistics hybrids, however, is bad. Hybrids often have strong starts. The playbooks are often similar:

Position as a technology company

Raise money at premium valuations

Use that money to buy growth and market share

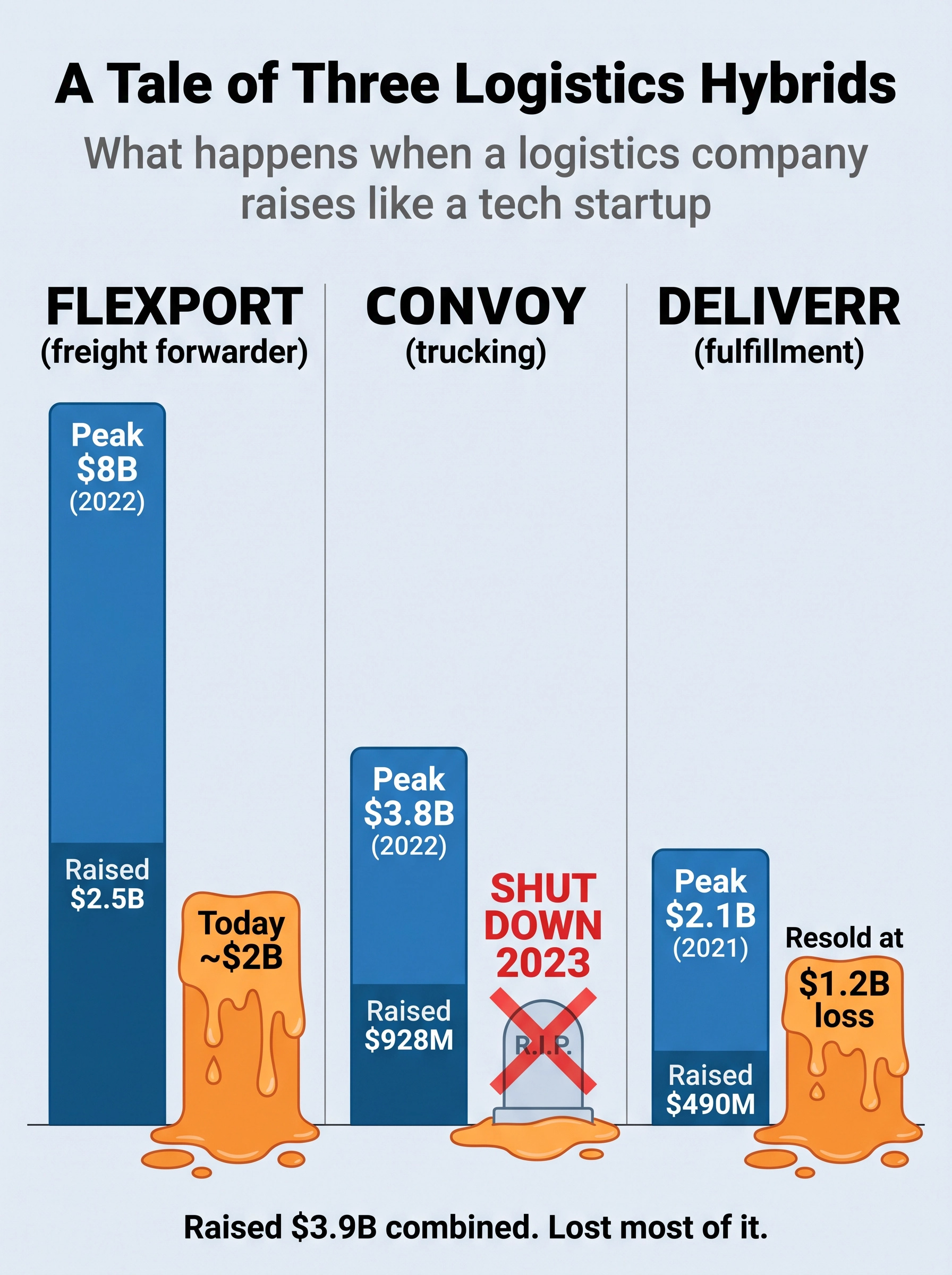

A Tale of Three Logistics Hybrids

The problem is that using money to buy growth and marketshare is not sustainable. At some point growth decelerates, and once the allure of being a high growth tech startup vanishes, valuations come crashing down to earth. What previously looked like a tech company ends up looking like a logistics company with great in-house tech and R&D, and that’s not good for valuations.

Flexport - Freight Forwarder

Raised: $2.5B | Peak Valuation $8B in 2022

Today estimated worth about $2B

Convoy - Trucker

Raised: $928M | Peak Valuation $3.8B in 2022

Shut down, dissolved

Deliverr - Fulfillment

Raised: $490M | Peak Valuation $2.1B in 2021

Resold later at a $1.2B loss, and today likely has lost significantly more value

Do Unicorns Exist?

“Leave it to the Chinese. I didn’t think it was possible.”

- Carl Anheuser, from the movie “2012”

If there are any examples of logistics technology hybrids that absolutely dominate, it would be China’s Cainiao and JD Logistics. Both companies unmistakably are in the business of providing and operating ecommerce logistics services, but the moment you check under the hood, it becomes abundantly clear that these companies are genuinely technology companies that develop their own software, hardware, and apply AI and data science to orchestrate logistics better than any traditional logistics company could - and they are crushing it globally.

The circumstances for both companies are hard to replicate. Cainiao is part of Alibaba Group, China’s largest ecommerce. JD Logistics spun out of JD.com, China’s 2nd largest ecommerce retailer with $182B in revenue (not GMV, which would be significantly higher). In other words, both are spin outs of tech giants with huge resources and talent pools, and also cut their teeth in the largest and most competitive ecommerce market in the world.

Where are we going?

With 8 acquisitions, $325M in fresh capital, and a $1.5B valuation, Stord may seem unstoppable to an undiscerning eye. The strategy is working for now, but growth through acquisitions rooted in valuation arbitrage and dependent on further fundraising is risky.

Every acquisition adds revenue but also adds operational complexity, integration risk, and makes it look less like the pure tech play that justifies its valuation premium. At some point, investors may just see a logistics company with in-house tech and price it accordingly.

Whether Stord can or even wants to go the true orchestration route like Cainiao side is not clear, but if it wants to sustain it’s momentum, it needs to show investors growth, and in an industry where the sales cycle can be 2 years, it might not have many options but to continue down it’s acquisitions path.

If you enjoyed this analysis, you’ll love what’s coming. Please make sure you’re subscribed so that you' don’t miss a beat.