All Roads Lead to Post-Purchase

Tracking and Returns are the latest celebrity couple

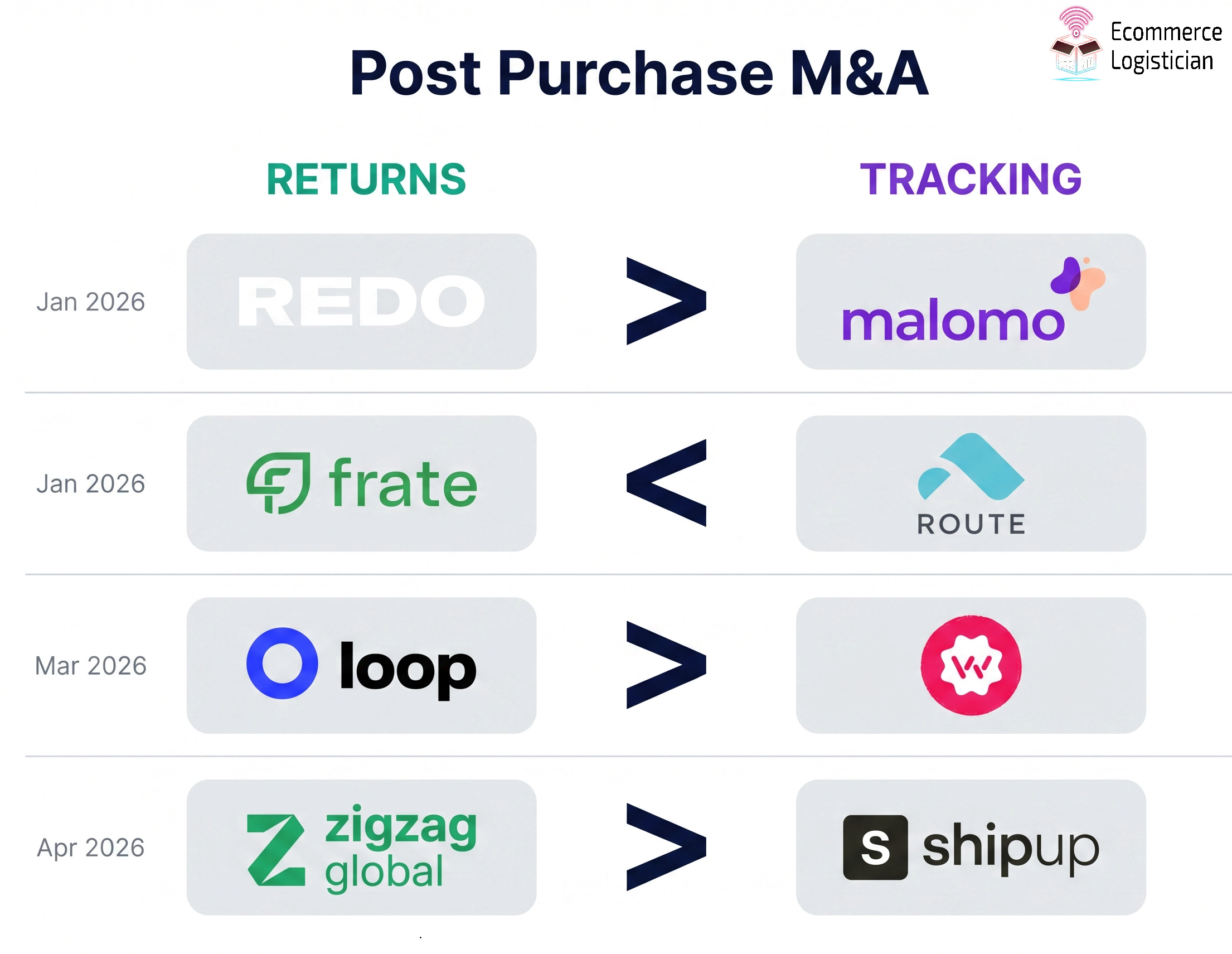

Something peculiar is happening in the ecommerce SAAS tracking and returns space. The the past 4 months, a flurry of consolidation has taken place.

Jan 2026 | Redo (Returns) acquires Malomo (Tracking)

Jan 2026 | Route (Tracking) acquires Frate (Returns)

Mar 2026 | Loop (Returns) acquires Wonderment (Tracking)

Apr 2026 | ZigZag Global (Returns) acquires Shipup (Tracking)

Why is this happening? Is merging tracking with returns just the latest fad? Or are the two destined for matrimony? To understand this, let’s go back to where it all started.

2021: The Gold Rush for Returns

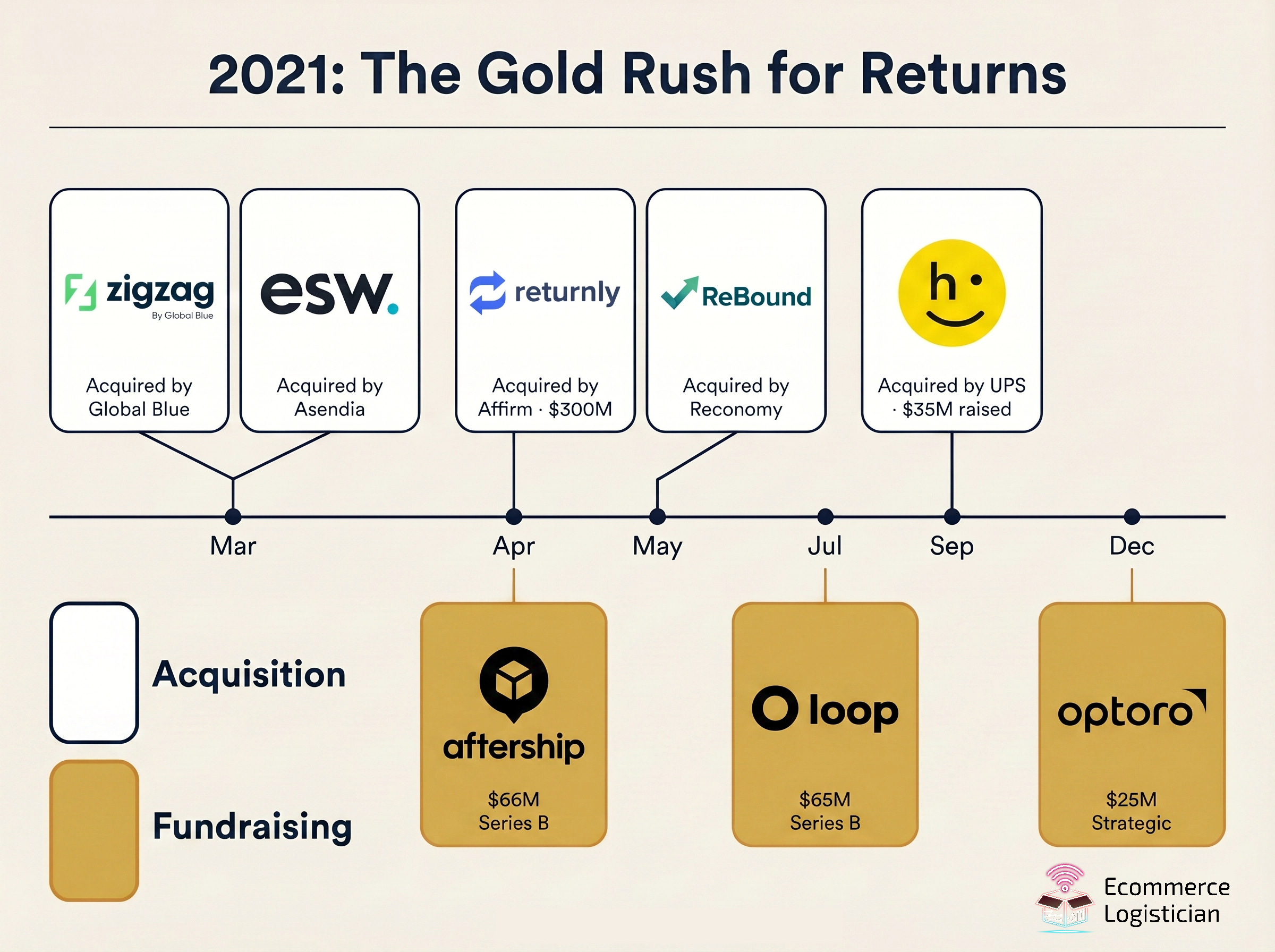

Returns Management Solutions (RMS) first catapulted into the spotlight during the Covid ecommerce boom. Investors bet big that the boon in ecommerce coming from shoppers-stuck-at-home would result in a corresponding surge of returns as well. Combine that with frothy valuations and 2021 officially became the Gold Rush for Returns.

2021 Returns Acquisitions

Mar 2021 | ZigZag acquired by BlueGlobal

Mar 2021 | eShopWorld acquired by Asendia

Sep 2021 | Happy Returns ($35M raised) acquired by UPS

Apr 2021 | Returnly ($50M raised) acquired by Affirm for $300M

May 2021 | Rebound acquired by Reconomy

2021 Returns Fundraising

Apr 2021 | AfterShip $66M Series B

Jul 2021 | Loop $65M Series B

Dec 2021 | Optoro $25M strategic led by Zebra

One at the time, the remaining companies were spoken for as well:

Nov 2023 | Doddle acquired by Blue Yonder

Aug 2023 | Optoro acquired by Blue Yonder

Jan 2025 | Inmar Returns acquired by DHL Supply Chain

Jul 2025 | ReturnGo acquired by Global-e

Post Purchase: The Ugly Duckling

Early investors, founders, and management teams likely believed that the returns industry was forecasted to grow so big - $850 billion in 2025 according to NRF - that multiple pure play returns companies could become unicorns.

While pure play returns companies received press and funding, a slew of other post-purchase companies were also quietly building by the sidelines. Post-purchase simply refers to anything after-the-purchase and can cover a large number of things, including shipping labels, tracking & shipment notifications, claims & insurance, and returns & warranty.

Some companies in the post-purchase space such as AfterShip, Narvar, Parcel Perform, Parcel Labs, and NShift, approached the problem-solution holistically, viewing each individual function of post-purchase as integrated components of a total solution.

This laid the foundation of infographics and marketing collateral from these companies for years to come: Pure Play vs Full Suite.

If a retailer would looking for a returns management solution, for example, they would likely be funnelled into a decision tree of either selecting a pure play returns solution like Loop, or going with a full suite post-purchase solution like Narvar.

Pure Play vs Full Suite

Some challenges a pure play returns or pure-play-anything might face include:

Merchants suffer from app fatigue (aka app sprawl) and don’t want to have 20 apps installed to manage their ecommerce business - this speaks to operations, training, integration, analytics, procurement and direct cost of multiple apps

Returns are preceded by shipping and tracking, meaning that without shipping or tracking in place, pure play returns companies are entrenching other post-purchase solution providers into the merchant’s ecom stack. These other solution providers can then cross-sell their competition returns-management-system (RMS) to the merchant, before the pure returns player even has a chance to pitch.

Pricing flexibility. As mentioned early, the direct cost of splitting up post purchase into multiple apps can be costly. Having multiple products under a single suite allows post purchase to have more flexibility to customize their pricing to fit the situation. Just the options of blending or bundling makes a dramatic difference

Conversely, pure returns players can have great advantages as well:

Best in class product

100% dedication of company focus to a single product

Clearer and simpler product marketing, messaging, and positioning

So which strategy is correct?

There Can Be Only One

SAAS is a business where eventually the big eat the small. Bigger typically means more resources. More engineers, more product managers, more support, more marketing, more sales. Finding a nice solid niche to enter a market, and then successfully executing takes hard work, skill, and luck.

However, in the SAAS game where KPIs like Average Contract Values (ACVs), Average Revenue Per User (ARPUs), and Revenue Per Employee (RPE) need to constantly climb, players will eventually get to a point where the next logical expansion is to cover another area of the post-purchase space.

Therefore while the advantages of being a pure-player in post-purchase can be compelling initially, the recent groundswell of returns + tracking mergers seems to indicate that the market is maturing. The initial land grab from the Gold Rush is slowing, and players are now moving towards post-purchase as a single unified solution.

If you’re interested in Ecommerce Logistics, subscribe now to get the latest updates.